Every year, airlines and hotels give away billions of dollars in free travel. Most people never collect a single cent of it.

That's not because they can't. It's because nobody explained the system.

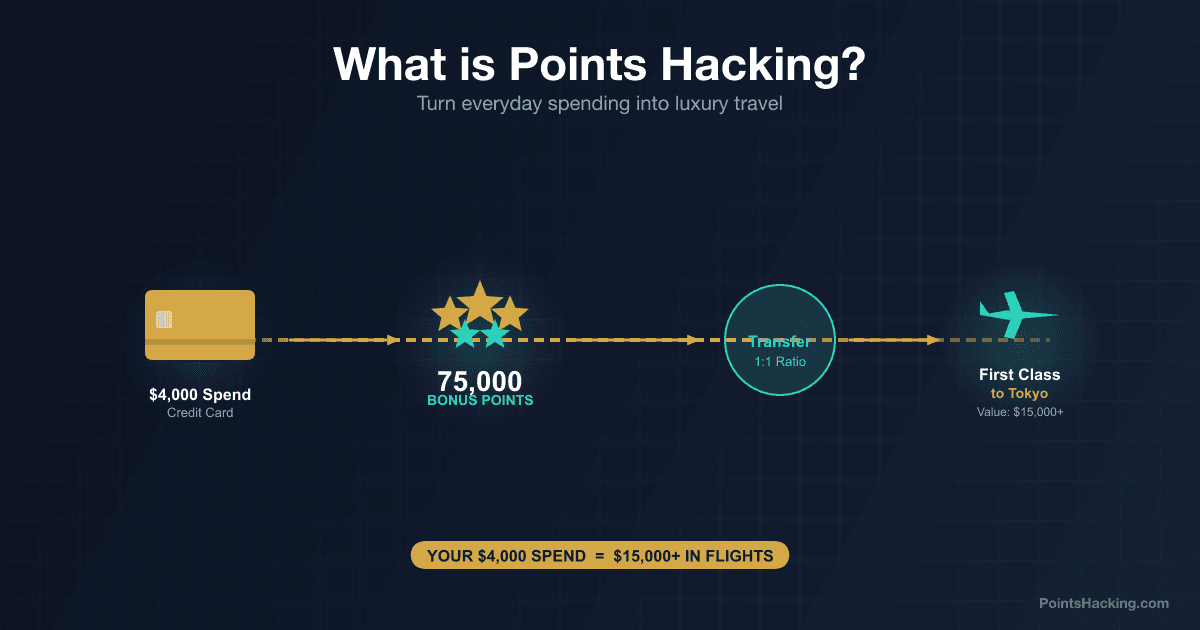

Points hacking is the practice of strategically earning and redeeming loyalty points and miles to unlock outsized travel value — business class flights, five-star hotel rooms, airport lounge access — at a fraction of the cash price or completely free. We're talking about a business class seat to Tokyo that costs $8,000 in cash but only 60,000 points. A $500-per-night hotel room redeemed for 15,000 points. A first-class upgrade booked with a sign-up bonus you earned by opening one credit card and spending normally for three months.

This guide covers everything you need to understand the loyalty points ecosystem from the ground up: why it exists, how the math works, how to earn points without changing your lifestyle, and how to redeem them for maximum value. By the end, you'll have a clear picture of exactly how to get started.

The Loyalty Points Ecosystem Explained

Before you earn a single point, you need to understand why this system exists and who benefits from it. The loyalty industry is a multi-billion-dollar financial ecosystem where banks, airlines, hotels, and consumers all have something to gain — but consumers have to know the rules to capture their share.

Why banks create reward programs: Every time you swipe a credit card, the merchant pays an interchange fee of 1.5–3% to the bank. On a $100 grocery run, the bank collects $1.50 to $3.00. Premium rewards cards charge merchants higher interchange because their cardholders spend more. Banks share a portion of that fee with you as points. The more you spend on their card, the more profitable you are as a customer — and the more they're willing to pay you in points to keep using their card.

Why airlines sell miles cheaply to banks: Airlines sell miles to banks in bulk at roughly 1–1.5 cents each. Banks then distribute those miles to cardholders as rewards. For airlines, it's pure revenue — they collect cash today for miles that may never be redeemed, and when they are redeemed, it costs the airline far less than the equivalent cash ticket because award seats are often on flights that would otherwise fly with empty seats.

Credit Card Issuers (Chase, American Express, Capital One, Citi, Bilt) issue cards that earn "transferable points" — flexible currencies that can be sent to multiple airline and hotel partner programs. This is where the leverage lives.

Airline Programs (United MileagePlus, Delta SkyMiles, American AAdvantage, Air France Flying Blue) let you book award flights using miles. You earn miles by flying, by using co-branded credit cards, or by transferring points from credit card programs.

Hotel Programs (World of Hyatt, Marriott Bonvoy, Hilton Honors) work the same way: earn points from stays or credit card spending, redeem for free nights and upgrades.

Transfer Partners are the bridge that makes everything possible.

Transfer Partners are the bridge that makes everything possible. Chase Ultimate Rewards transfers to United, Hyatt, British Airways, and 11 other partners at a 1:1 ratio. American Express Membership Rewards transfers to Delta, Air France Flying Blue, Marriott, Singapore Airlines, and 18+ others. When you earn 80,000 Chase points as a sign-up bonus, you are not locked into one airline. You can send those points wherever the best deal exists at the moment you're ready to book.

For a deep dive into which card programs offer the best transfer partner networks, read our Chase Ultimate Rewards complete guide.

Why Points Hacking Works: The Real Math

The fundamental insight of points hacking is this: airlines price award seats using a completely different formula than they use for cash tickets. And that discrepancy is where points hackers make their money.

A business class seat from New York to London might cost $4,500 in cash. In points, that same seat might cost 57,500 Amex Membership Rewards points via Air France Flying Blue — and Flying Blue runs monthly Promo Rewards sales that discount partner routes by 25–50%, bringing that number below 40,000 during sale periods.

If you earned those 57,500 points from a single credit card sign-up bonus — which typically requires spending $4,000–$6,000 in the first three months — you effectively traded your normal grocery, gas, and restaurant spending for a $4,500 international business class flight.

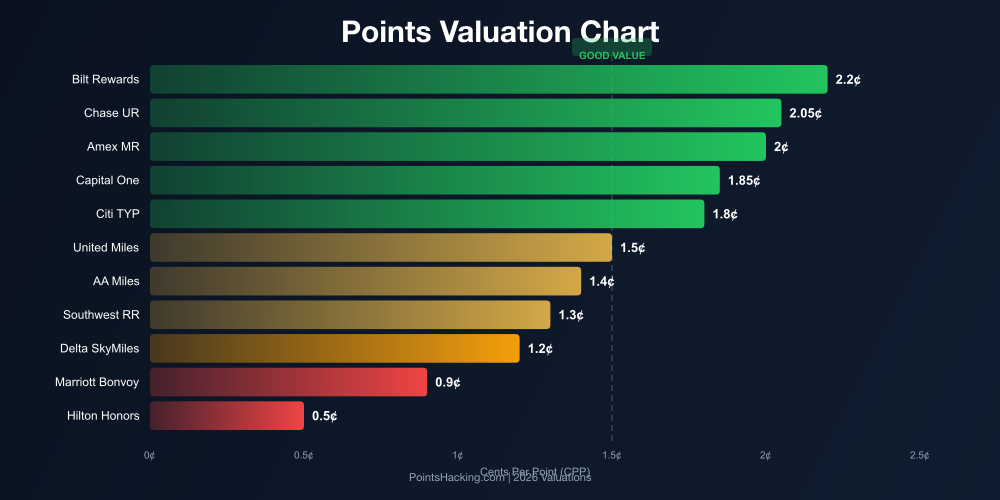

The key metric is cents per point (CPP). When you redeem 57,500 points for a $4,500 flight, you're extracting 7.8 cents per point. A typical sign-up bonus is 60,000–80,000 points. At 7.8 CPP, that's $4,680–$6,240 in real travel value from a single bonus.

Contrast that with the baseline: most points are worth 0.5–1 cent each when cashed out for statement credits. By chasing the right redemptions, you get 5–20x more value from the same points.

The 4 Main Ways to Earn Points

You don't need to be a frequent flyer or a big spender to earn points. The four earning methods below are available to almost anyone with a credit card and a checking account.

1. Credit Card Sign-Up Bonuses — This is the fastest path to free travel by a wide margin. A card like the Chase Sapphire Preferred offers 60,000 points after spending $4,000 in the first three months. At 5 cents per point in a good redemption, that's $3,000 in travel value. The American Express Gold card has offered 60,000–90,000 Membership Rewards points on elevated offers. Capital One Venture X regularly offers 75,000 miles. These bonuses are the single biggest driver of value in the entire hobby.

The key: you don't need to spend extra money to hit minimum spend requirements. Simply redirect your existing spending — groceries, gas, restaurants, subscriptions, utilities — to the new card for three months. Most households spend $3,000–$5,000 per month naturally.

2. Category Multipliers on Everyday Spending — Beyond sign-up bonuses, premium cards offer elevated earn rates on specific categories. The Amex Gold earns 4x Membership Rewards at restaurants worldwide and at U.S. supermarkets. The Chase Sapphire Reserve earns 4x on direct hotel and flight purchases. The Citi Strata Premier earns 3x on flights, hotels, restaurants, supermarkets, and gas stations simultaneously. Stack the right cards against your spending profile and you can earn 3–5 points per dollar on most of your monthly expenses.

3. Shopping Portals and Partner Bonuses — Airlines and credit card issuers operate online shopping portals that let you earn bonus points when you make purchases through them. Buy something at Nike through the United MileagePlus Shopping portal and earn 5 extra miles per dollar — on top of whatever your credit card earns. Chase has the Chase Ultimate Rewards shopping portal. Amex has Amex Offers, which provide statement credits and bonus points at hundreds of retailers. These cost nothing and stack with credit card rewards.

4. Airline and Hotel Direct Stays — When you fly United, you earn United miles. When you stay at a Hyatt property, you earn World of Hyatt points. If you travel frequently for work, these direct earning streams compound quickly — especially if you achieve elite status, which provides bonus point multipliers on every stay or flight. However, for people who don't travel frequently already, direct earning from flights and hotels is the slowest method and should be supplementary, not primary.

The optimal strategy combines all four: earn a sign-up bonus, use category multipliers for ongoing spending, click through shopping portals when buying online, and credit your hotel stays and flights to the right programs. Read our guide on the best travel credit cards of 2026 to understand which cards cover which categories best.

The 3 Redemption Tiers: Ranked by Value

Not all point redemptions are created equal. The difference between the best and worst redemption options is 10x or more in value. Here's the hierarchy you need to internalize before you transfer a single point.

Tier 1: Premium International Awards (Best Value, 5–20+ CPP)

Business class and first class redemptions using airline transfer partners consistently deliver the highest cents-per-point value available. A $10,000 ANA First Class "The Suite" seat from New York to Tokyo costs 55,000 Virgin Atlantic Flying Club miles — and you can transfer Chase Ultimate Rewards or Amex Membership Rewards to Virgin Atlantic at a 1:1 ratio. That's 18+ cents per point. A $6,000 Lufthansa business class seat can be booked through Aeroplan for 65,000 points, delivering 9+ CPP. These redemptions are where points hacking separates from every other form of loyalty optimization.

Tier 2: Economy International Awards and Hotel Sweet Spots (Good Value, 1.5–4 CPP)

International economy sweet spots can still hit 1.5–2 cents per point. Flying Blue Promo Rewards sometimes prices transatlantic economy as low as 12,000 points one-way — a ticket that costs $600 in cash. That's 5 CPP in economy, which outperforms most business class redemptions. World of Hyatt consistently delivers 1.8–2.5 CPP on hotel redemptions, particularly at all-inclusive properties where points cover food and drinks in addition to the room. These mid-tier redemptions are accessible, predictable, and excellent for most travelers.

Tier 3: Domestic Economy, Statement Credits, Gift Cards (Worst Value, 0.5–1 CPP)

If you redeem your Chase Ultimate Rewards for 1 cent each as cash back, or your Amex points for gift cards at 0.7 cents each, you are leaving 80–90% of the value on the table. Domestic economy flights booked with points at face value are slightly better but still pale in comparison to Tier 1 and 2 options. Never cash out transferable points unless you have exhausted all other options.

5 Common Points Hacking Myths Debunked

Points hacking has a reputation for being complicated, risky, or only accessible to wealthy frequent flyers. All of these perceptions are wrong. Here are the five most common myths and why they don't hold up.

Myth 1: "I need perfect credit to get started." You need good credit, not perfect credit. The Chase Sapphire Preferred — the ideal starter card — approves applicants with scores around 700 or above. If your score is below that, spend three to six months paying down balances and keeping utilization below 10% before applying. Most people with responsible financial habits qualify.

Myth 2: "Points hacking is only for frequent business travelers." This is completely backwards. Frequent business travelers are often locked out of the best sign-up bonuses because they've already opened those cards through their companies. Points hackers earn the bulk of their points from credit card spending at the grocery store, restaurants, and gas stations — not from flights. You can earn a first-class international redemption without ever setting foot in an airport before the trip.

Myth 3: "It's too complicated." The basics are genuinely simple. Open one transferable-points credit card. Earn the sign-up bonus through normal spending. Identify a specific trip you want. Transfer points to the relevant airline or hotel partner. Book the award. That's the entire system. Everything beyond that — stacking cards, optimizing transfer partners, hunting transfer bonuses — is optional optimization, not a prerequisite.

Myth 4: "Points expire and I'll lose them." Most transferable credit card points (Chase UR, Amex MR, Capital One Miles, Citi ThankYou) do not expire as long as your account is open and in good standing. Some airline miles have activity-based expiration (usually 18–24 months of inactivity), which is easily reset by making a single small purchase or transfer. Hotel points tend to expire after 12–24 months of inactivity, but a single redemption resets the clock.

Myth 5: "I'll get into debt." Points hacking only works if you pay your balance in full every month. Carrying a balance and paying 22% APR interest instantly destroys any value the rewards provide. If you have any tendency to carry a balance, build that habit first before applying for rewards cards. The system is designed for people who use credit cards as a payment tool, not as a borrowing tool.

For more on why transfer partners are the key to unlocking maximum value, read our post: Never Buy Points With Your Credit Card — Always Transfer.

Getting Started: Your First 5 Steps

You don't need to master the entire ecosystem before taking action. Here is the exact sequence that gets you from zero to your first free flight or hotel stay.

Step 1: Check your credit score. Pull your free score from Credit Karma or your bank's portal. If you're above 700, you're eligible for most premium travel cards. If not, spend a few months paying down balances and then revisit.

Step 2: Open one transferable-points credit card. If you're new to the hobby, start with the Chase Sapphire Preferred ($95 annual fee, 60,000+ point bonus). Chase has strict 5/24 rules — if you've opened 5+ personal cards in the last 24 months, you're ineligible. Get Chase cards first. For a full breakdown of the Chase ecosystem, see our Chase Ultimate Rewards complete guide.

Step 3: Use the card for everything for three months. Hit the minimum spend organically — groceries, gas, subscriptions, dining, utilities. Do not put spending on the card you can't pay off when the statement arrives.

Step 4: Identify your first award trip before you transfer anything. Search for award availability on partner programs. Confirm the seat or room exists before you transfer a single point. Transfers are irreversible.

Step 5: Transfer your points and book. Once you have confirmed availability, transfer exactly the number of points you need and book immediately. Award seats evaporate. Don't wait.

That's the entire system in five moves. You can do all of this in your first three months. Everything beyond that — stacking multiple cards, building point portfolios across programs, hunting transfer bonuses — is how you go from one free trip to five or ten per year. But you don't need to do any of it to get started.

According to NerdWallet's beginner points guide, the average household can realistically earn enough points for one to two free international flights per year simply by redirecting everyday spending to a rewards card and earning the sign-up bonus.

The people flying business class to Tokyo on points aren't a different type of traveler. They just learned the rules of a game that banks and airlines set up decades ago — and they're playing it.