The Chase Sapphire Preferred and the Citi Strata Premier are two of the most popular mid-tier travel credit cards on the market. Both carry a $95 annual fee, both earn transferable points, and both offer solid earning rates across travel and dining. But they belong to different ecosystems, serve different transfer partner networks, and reward different spending patterns. This comparison will help you decide which card belongs in your wallet — or whether you should carry both.

For deeper context on each ecosystem, see our Chase Ultimate Rewards complete guide before deciding. Understanding how each currency transfers and which partners matter most to your travel style is the foundation of this decision.

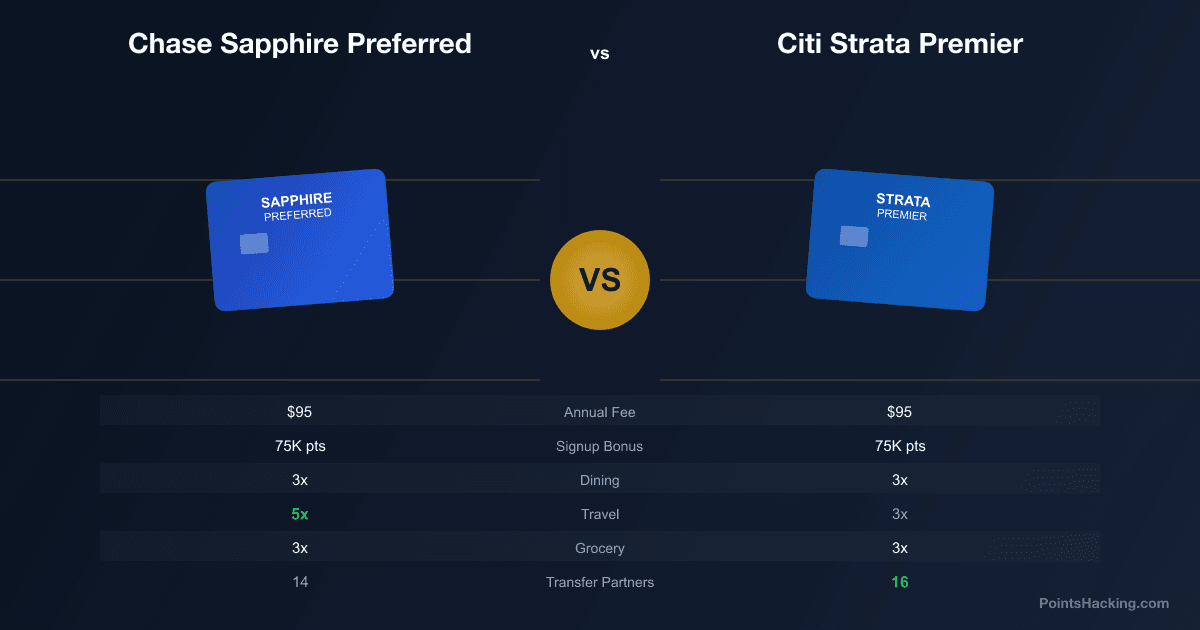

Annual Fee and Welcome Bonus

Both cards charge a $95 annual fee, making them direct competitors in the mid-tier segment. Neither charges foreign transaction fees.

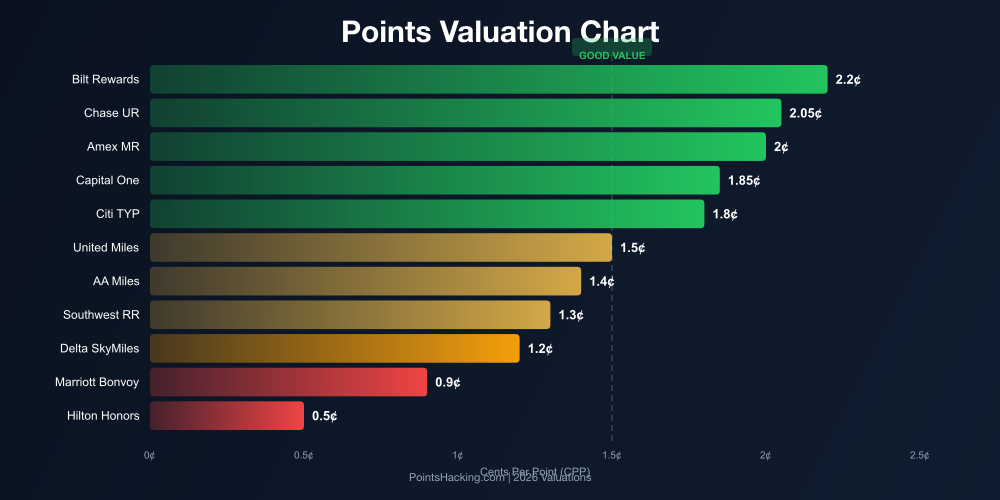

The Chase Sapphire Preferred typically offers a welcome bonus in the 60,000-to-80,000 Ultimate Rewards point range after spending $4,000 in the first three months. At our valuation of 2.05 cents per point, a 60,000-point bonus is worth approximately $1,230. The card also includes a $50 annual hotel credit applied as a statement credit when you book through the Chase Travel portal, partially offsetting the annual fee.

The Citi Strata Premier typically offers a welcome bonus of 60,000-to-75,000 ThankYou points after spending $4,000 in the first three months. At our valuation of 1.8 cents per point, a 60,000-point bonus is worth approximately $1,080. Citi does not include a hotel credit or other annual benefit to offset the fee, though the card's earning rates are stronger in several categories.

Verdict on bonuses: Chase edges out slightly on first-year value when you factor in the hotel credit, but both bonuses are competitive and the gap is modest. The bigger differentiator is the long-term earning structure.

Earning Rates: Where Each Card Shines

The Citi Strata Premier has one of the strongest category earning structures of any $95 annual fee card on the market:

- 3x ThankYou points on air travel, hotels, restaurants, groceries, and gas stations

- 1x ThankYou points on all other purchases

That five-category 3x earning structure is exceptional. Most mid-tier cards offer 3x or more on two to three categories; the Strata Premier covers five, including groceries and gas — spending categories that can drive thousands of bonus points per year for the average household.

The Chase Sapphire Preferred earning structure:

- 5x Ultimate Rewards points on travel purchased through Chase Travel

- 3x on dining (including eligible delivery services)

- 3x on online grocery purchases (excluding Target, Walmart, wholesale clubs)

- 3x on select streaming services

- 2x on all other travel purchases

- 1x on all other purchases

The Sapphire Preferred's 5x on Chase Travel bookings is powerful if you book through the portal, but 2x on general travel is lower than Citi's 3x on air and hotels booked directly. For travelers who prefer to book directly with airlines and hotels — which is often better for elite status and upgrade eligibility — the Strata Premier wins on travel earning.

For dining and groceries, the two cards are essentially tied at 3x. The Strata Premier adds gas at 3x, which is a meaningful edge for cardholders who drive regularly. The Sapphire Preferred's streaming credit is a niche benefit that few cardholders maximize.

Transfer Partners: The Defining Difference

Transfer partners are where the two ecosystems diverge most significantly, and this is the single most important factor for serious points collectors.

Chase Ultimate Rewards transfers to 14 airline and hotel partners including United Airlines, Southwest Airlines, British Airways, Air France/KLM Flying Blue, Singapore Airlines KrisFlyer, Emirates Skywards, Aer Lingus, Iberia, Virgin Atlantic, Air Canada Aeroplan, Turkish Airlines Miles&Smiles, and IHG One Rewards, World of Hyatt, and Marriott Bonvoy. All transfers are 1:1 with no fees. Most transfer in real time.

Citi ThankYou transfers to 17+ airline partners including Air France/KLM Flying Blue, Turkish Airlines Miles&Smiles, Singapore Airlines KrisFlyer, Virgin Atlantic Flying Club, Avianca LifeMiles, Cathay Pacific Asia Miles, Emirates Skywards, Etihad Guest, Eva Air Infinity MileageLands, and several others. Notably, Citi does not transfer to United, Southwest, British Airways, or World of Hyatt — the four Chase partners that travel hackers value most.

However, Citi has exclusive or advantageous access to partners that Chase lacks, including Avianca LifeMiles (fantastic for Star Alliance awards at low rates), Turkish Airlines Miles&Smiles (exceptional for United flights booked at Turkish rates), and Cathay Pacific Asia Miles. These partners can unlock extraordinary value for premium cabin international bookings.

Bottom line on transfer partners: Chase wins for domestic US travel (United, Southwest), luxury hotel redemptions (Hyatt), and British Airways Avios for short-haul. Citi wins for certain international premium cabin redemptions and for travelers already invested in airlines like Air France or Avianca.

For a full breakdown of where each currency delivers the most value, see our best travel credit cards 2026 overview.

Travel Protections and Perks

This is a clear win for the Chase Sapphire Preferred. Chase has historically offered some of the strongest travel protections of any mid-tier card:

- Trip cancellation/interruption insurance: Up to $10,000 per person, $20,000 per trip

- Trip delay reimbursement: Up to $500 per ticket for delays over 12 hours

- Baggage delay insurance: Up to $100 per day for up to 5 days

- Auto rental collision damage waiver: Primary coverage (pays before your personal insurance)

- Purchase protection: Up to $500 per claim, $50,000 per account

- Extended warranty protection: Extends manufacturer warranties by one year

The Citi Strata Premier offers:

- Trip cancellation/interruption insurance: Up to $5,000 per trip

- Trip delay protection: Up to $500 per covered trip for delays over 6 hours (better threshold than Chase)

- Lost or damaged luggage: Up to $3,000 per trip

- Auto rental collision damage waiver: Secondary coverage

- Purchase protection and extended warranty

Chase's primary auto rental coverage is a meaningful practical advantage. Secondary coverage, which Citi offers, requires you to file with your personal auto insurance first — adding hassle and potentially affecting your rates. For frequent car renters, Chase's primary coverage alone can justify the card.

Who Each Card Is Best For

The Chase Sapphire Preferred is the better choice if you value strong travel protections, want access to World of Hyatt and United Airlines transfer partners, book car rentals frequently, or are building toward a Chase trifecta. It is also the better choice if you already have Chase business cards like the Ink cards, since pooling points into a Sapphire account unlocks transfer partner access.

The Citi Strata Premier is the better choice if you spend heavily on groceries, gas, and air travel booked directly, want to access Avianca LifeMiles or Turkish Airlines Miles&Smiles for premium international redemptions, or are building a Citi trifecta. Its flat 3x on five categories makes it a simpler, broader earning machine for everyday spending.

Review your own credit profile and application history before applying for either card. Our credit card application order strategy guide explains how to approach applying for both Chase and Citi cards without triggering denials or burning unnecessary hard pulls.

Can You Have Both Cards?

Yes. Holding both the Chase Sapphire Preferred and the Citi Strata Premier is a legitimate strategy for maximizing rewards across two separate ecosystems. There are no rules preventing you from holding cards from competing banks simultaneously.

The dual-card approach makes sense if you have travel goals that benefit from both partner networks — for example, United flights (Chase) and Avianca LifeMiles redemptions (Citi) — or if you want to maximize category bonuses across both systems. Your Chase cards cover one set of transfer partners; your Citi cards cover another.

One important note: Chase has a one-Sapphire-product rule, meaning you cannot hold the Sapphire Preferred and Sapphire Reserve simultaneously. You must choose one. Citi has no equivalent restriction on their ThankYou-earning cards.

Trifecta Strategies for Each Ecosystem

The Chase trifecta pairs the Sapphire Preferred (or Reserve) with the Chase Freedom Unlimited and Chase Freedom Flex. The Freedom Unlimited earns 1.5x on everything; the Freedom Flex earns 5x on rotating quarterly categories (groceries, gas, dining, PayPal, and others). Both Freedom cards earn Chase Ultimate Rewards points that transfer to your Sapphire account for full partner access. This combination covers virtually every spending category at elevated rates.

The Citi trifecta pairs the Strata Premier with the Citi Double Cash (2x on everything — 1x when you buy, 1x when you pay) and the Citi Custom Cash (5x on your top spending category each month, up to $500 per month). The Double Cash earns ThankYou points that can be pooled with your Strata Premier account; the Custom Cash does as well. This combination gives you 5x on one key category, 3x on five categories from the Strata Premier, and 2x as a floor on everything else — a powerful earning structure with minimal category management.

For an independent perspective on both cards, Bankrate's credit card comparison tools provide regularly updated side-by-side analysis including current bonus offers and rate changes.

Frequently Asked Questions

Is the Chase Sapphire Preferred or Citi Strata Premier better for travel?

The Sapphire Preferred is generally better for domestic US travel (United, Southwest transfers, Hyatt hotels) and offers stronger travel protections including primary auto rental coverage. The Strata Premier is better for international premium cabin bookings via Avianca LifeMiles and Turkish Airlines, and earns more points on everyday categories like groceries and gas.

Which card has better transfer partners in 2026?

Chase Ultimate Rewards has more partners that US-based travelers use most often, including United, Southwest, British Airways, and World of Hyatt. Citi ThankYou has unique access to Avianca LifeMiles and Cathay Pacific that can unlock exceptional international redemption value not available through Chase.

Can I hold both the Chase Sapphire Preferred and the Citi Strata Premier?

Yes. There is no rule preventing you from holding both cards simultaneously. Many advanced points collectors maintain both to access both transfer partner networks and maximize category earning.

Does the Citi Strata Premier have travel insurance?

Yes. The Strata Premier includes trip cancellation and interruption insurance up to $5,000, trip delay protection for delays over 6 hours, lost luggage coverage, and secondary auto rental collision damage waiver. Chase's protections are generally more comprehensive, particularly for auto rentals where Chase offers primary coverage.

What is the annual fee for the Chase Sapphire Preferred and Citi Strata Premier?

Both cards carry a $95 annual fee with no foreign transaction fees. The Sapphire Preferred partially offsets this with a $50 annual hotel credit through Chase Travel; the Strata Premier does not include an equivalent offsetting benefit but compensates with broader category earning rates.